The Corporate Sustainability Reporting Directive (CSRD) is an initiative by the European Union (EU) to align sustainability reporting with financial reporting, set to be phased in starting in 2024:

Which companies are impacted?

All large companies established in an EU Member State that meet 2 or more of the below requirements will be subject to CSRD:

-

- €40 million in net turnover;

- €20 million on the balance sheet;

- 250 or more employees.

What are the timelines for implementation?

CSRD will impact entities in a phased approach:

-

- Large companies already subject to the Non-Financial Reporting Directive (NFRD) will be impacted first: from 2024, with their first CSRD-compliant annual report published in 2025.

- Large companies not subject to the NFRD will then need to comply from 2025, with their first annual CSRD-compliant annual report published in 2026.

- Listed SMEs will also be in scope from 2026, with their first annual CSRD-compliant report published in 2027. An opt-out may be possible for listed SMEs, exempting them from reporting until 2028.

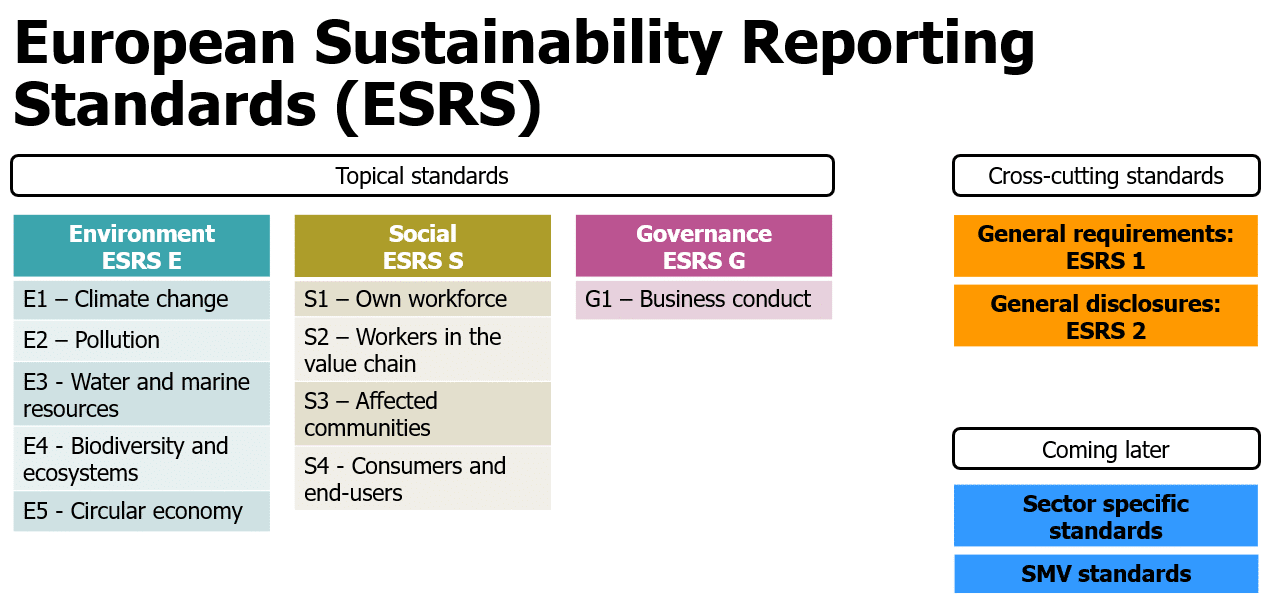

Reporting Structure:

Show full Reporting Structure PDF – Corporate Sustainability Reporting Directive (CSRD)

Examples of data for CSRD reporting

Anti-corruption and Bribery:

-

- Anti-corruption Policies: Description of anti-corruption policies, training, and compliance monitoring.

- Incidents of Corruption: Number of confirmed incidents and actions taken in response.

- Legal Compliance: Fines and other sanctions for non-compliance with laws and regulations.

Diversity on Company Boards:

-

- Board Diversity: Breakdown of board members by gender, age, ethnicity, educational and professional background.

- Diversity Policies: Description of diversity and inclusion policies, objectives, and outcomes.

Governance Factors:

-

- Corporate Governance Structure: Description of the governance structure, roles, and responsibilities.

- Ethical Conduct: Description of code of ethics, ethical conduct training, and monitoring.

Additional Reporting:

-

- Science-Based Targets: Progress towards science-based targets for reducing greenhouse gas emissions.

- Climate Risk-Related Reporting: Assessment of climate-related risks and opportunities, and strategies to address them.

Environmental Matters:

-

- Greenhouse Gas Emissions: Total emissions, emissions intensity, and reductions.

- Energy Consumption: Total energy consumption, energy efficiency measures, and renewable energy usage.

- Water Usage: Total water withdrawal, water recycling rates, and water-saving measures.

- Waste Management: Total waste generated, recycling rates, and waste disposal methods.

Social Matters and Treatment of Employees:

-

- Employee Health and Safety: Accident rates, occupational diseases, and safety training.

- Employee Training and Education: Training hours per employee, programs for skill management, and lifelong learning.

- Labor Practices: Collective bargaining agreements, employee turnover rates, and employee satisfaction surveys.

- Community Engagement: Community development programs, local hiring, and charitable contributions.

Respect for Human Rights:

-

- Human Rights Due Diligence: Policies, processes, and outcomes of human rights assessments.

- Supply Chain Management: Supplier assessments on human rights, and actions taken against suppliers violating human rights.

- Discrimination and Harassment: Number of incidents and actions taken to prevent discrimination and harassment.